finance

For Members

What to know about starting your personal banking in Germany

Amanda Pridmore - [email protected]

Published: 16 May, 2018 CET.

Updated: Wed 16 May 2018 11:44 CET

What with the potential language barriers and legal hold ups, choosing the right bank and opening the right account can be tricky in a foreign country. We give you all the insight you need on where to start when it comes to banking in Germany.

This article is available to Members of The Local. Read more Membership Exclusives here.

Germany is a banking powerhouse, with established names like Deutsche Bank, Commerzbank, KfW and DZ Bank all calling Germany home. With these big names, though, come a lot of differences in the banking structure. So how do you know where to start?

We walk you through the ins and outs of making your way through the German banking system.

Know the lingo

The first step to banking is knowing the lingo. Geldautomat, for example, is extremely important: ATM. Photo: DPA

Before you embark on navigating the complicated waters of banking in Germany, it’s important to know the lingo. Here are some of the important German-specific words that you will need to know before you set foot inside a German bank.

EC-Karte – This is an EC card, essentially the same as a debit card, that is the most accepted form of credit payment by most German retailers.

IBAN and BIC- Much like in other places in Europe, your International Bank Account Number (IBAN) and Bank Identifier Code (BIC) are your account number and sort code written in a standard, internationally recognised format. The IBAN starts in Germany with the letters DE, which is the country identifier. Together, your IBAN and BIC will allow you to make international transfers.

Kontonummer– This is your individual account number at your given pack, which will be included as a part of your IBAN number. Equally important to know is your Bankleitzahl (BLZ) – this is your bank routing code, also contained within the IBAN number itself.

Überweisung/Geldüberweisung – This is the word for money transfer, which is how most people in Germany pay for larger bills. More on that later. Important to note in conjunction with this term is TAN codes – special transaction codes that you use online to verify payments from your account.

Picking the right account type

In order to make the right choice about how to begin your banking future in your new home country, it’s crucial to know the types of accounts available to expats in Germany. The two main categories of bank accounts: Girokonto and Sparkonto.

A Girokonto is essentially a checking account. Most transactions are done using this account type, and it works in conjunction with an EC card, as already mentioned. Unlike many countries, Germany does not have personal checks, and thus all transactions done from the Giro account are conducted using either the EC card, cash withdrawals or transfers.

A Sparkonto is the German equivalent of a savings account, and is often opened at the same time as the Giro account (though it can be opened later). This account allows you to save and collect interest.

With a Sparkonto, there is usually a limit on the amount of money you are allowed to withdraw per month, and money is not easily transferred into other accounts.

For both banking types, there are Kontoführungsgebühren, or bank account fees, depending on the institution.

Finding the right bank

The first step to banking is knowing the lingo. Geldautomat, for example, is extremely important: ATM. Photo: DPA

Before you embark on navigating the complicated waters of banking in Germany, it’s important to know the lingo. Here are some of the important German-specific words that you will need to know before you set foot inside a German bank.

EC-Karte – This is an EC card, essentially the same as a debit card, that is the most accepted form of credit payment by most German retailers.

IBAN and BIC- Much like in other places in Europe, your International Bank Account Number (IBAN) and Bank Identifier Code (BIC) are your account number and sort code written in a standard, internationally recognised format. The IBAN starts in Germany with the letters DE, which is the country identifier. Together, your IBAN and BIC will allow you to make international transfers.

Kontonummer– This is your individual account number at your given pack, which will be included as a part of your IBAN number. Equally important to know is your Bankleitzahl (BLZ) – this is your bank routing code, also contained within the IBAN number itself.

Überweisung/Geldüberweisung – This is the word for money transfer, which is how most people in Germany pay for larger bills. More on that later. Important to note in conjunction with this term is TAN codes – special transaction codes that you use online to verify payments from your account.

Picking the right account type

In order to make the right choice about how to begin your banking future in your new home country, it’s crucial to know the types of accounts available to expats in Germany. The two main categories of bank accounts: Girokonto and Sparkonto.

A Girokonto is essentially a checking account. Most transactions are done using this account type, and it works in conjunction with an EC card, as already mentioned. Unlike many countries, Germany does not have personal checks, and thus all transactions done from the Giro account are conducted using either the EC card, cash withdrawals or transfers.

A Sparkonto is the German equivalent of a savings account, and is often opened at the same time as the Giro account (though it can be opened later). This account allows you to save and collect interest.

With a Sparkonto, there is usually a limit on the amount of money you are allowed to withdraw per month, and money is not easily transferred into other accounts.

For both banking types, there are Kontoführungsgebühren, or bank account fees, depending on the institution.

Finding the right bank

With so many banks in Germany, picking the right one means weighing the benefits. Photo: DPA

Armed with your new German banking vocabulary and account knowledge, it’s time to figure out which of Germany’s plethora of banks is the right fit for you.

With so many options out there, it is good to know the big names in the German banking game. While there are many more than the ones below, here are some of the heavy hitters that you may want to keep on your radar.

Deutsche Bank – This is Germany’s largest bank, and is also one of the most well-known internationally. They offer a range of accounts designed for students and also professionals that hold client money in their private accounts. For our American readers, their partnership with Bank of America can make for easy money transfers for customers.

Commerzbank – One of the other large banks in the country, it offers a normal Giro account as well as premium accounts that offer two debit cards and travel insurance. Their site is available in English.

DKB – Deutsche Kredit Bank advertises itself as no/low fees and is an online banking service. It offers a free account and ATM withdrawals (unless that machine charges a fee). Customer support can be contacted via email or through a call centre. The downside perhaps is that they have no physical branches.

Sparkasse – Sparkassen have many branches and ATMs throughout Germany. Each large German city has its own Sparkasse, though in Berlin it is the largest retail/consumer bank in the city. However, they do have higher fees.

Location, location, location

One of the first factors to consider in choosing the right bank is your location in Deutschland. Are you in Berlin, where Sparkasse is the largest banking chain? Or maybe travelling between Frankfurt and Düsseldorf for work? Where you are can have a big affect on what bank is best for you, especially considering the high costs of withdrawing cash at competing banks.

A good rule of thumb in choosing a bank location is to find the three to five banks closest to your home or office, and use those as the start of your search.

Keep in mind that regional offerings, like Landesbank Baden-Württemberg, may not be available in other parts of Germany and might not be a good idea if you plan to travel frequently outside of your area.

Hidden fees

Another key component of selecting the right banking institution is to compare the possible fees. While each bank has its own unique charging rules, the big fees to look for come with age factors, withdrawing money from ATMs and international transfers.

German accounts typically cost around €10 per month in “maintenance fees”, though the exact number varies depending on the bank. Students are largely excempt from these monthly charges as long as they are under a certain age - at Commerzbank, for example, this includes students up to the age of 30.

Concerning withdrawing cash, the usual rule in Germany is that it is free to withdraw from your bank’s ATM, but it may cost you to grab a few bills from another location.

However, this is not universally the case. Berlin-favourite Sparkasse, for example, may charge its customers up to €0.50 for withdrawing money from their ATMs, even if they are Sparkasse customers. Other banks, like DKB, offer free withdrawals as long as the cash machine itself doesn’t require a fee.

Digital banking

With so many banks in Germany, picking the right one means weighing the benefits. Photo: DPA

Armed with your new German banking vocabulary and account knowledge, it’s time to figure out which of Germany’s plethora of banks is the right fit for you.

With so many options out there, it is good to know the big names in the German banking game. While there are many more than the ones below, here are some of the heavy hitters that you may want to keep on your radar.

Deutsche Bank – This is Germany’s largest bank, and is also one of the most well-known internationally. They offer a range of accounts designed for students and also professionals that hold client money in their private accounts. For our American readers, their partnership with Bank of America can make for easy money transfers for customers.

Commerzbank – One of the other large banks in the country, it offers a normal Giro account as well as premium accounts that offer two debit cards and travel insurance. Their site is available in English.

DKB – Deutsche Kredit Bank advertises itself as no/low fees and is an online banking service. It offers a free account and ATM withdrawals (unless that machine charges a fee). Customer support can be contacted via email or through a call centre. The downside perhaps is that they have no physical branches.

Sparkasse – Sparkassen have many branches and ATMs throughout Germany. Each large German city has its own Sparkasse, though in Berlin it is the largest retail/consumer bank in the city. However, they do have higher fees.

Location, location, location

One of the first factors to consider in choosing the right bank is your location in Deutschland. Are you in Berlin, where Sparkasse is the largest banking chain? Or maybe travelling between Frankfurt and Düsseldorf for work? Where you are can have a big affect on what bank is best for you, especially considering the high costs of withdrawing cash at competing banks.

A good rule of thumb in choosing a bank location is to find the three to five banks closest to your home or office, and use those as the start of your search.

Keep in mind that regional offerings, like Landesbank Baden-Württemberg, may not be available in other parts of Germany and might not be a good idea if you plan to travel frequently outside of your area.

Hidden fees

Another key component of selecting the right banking institution is to compare the possible fees. While each bank has its own unique charging rules, the big fees to look for come with age factors, withdrawing money from ATMs and international transfers.

German accounts typically cost around €10 per month in “maintenance fees”, though the exact number varies depending on the bank. Students are largely excempt from these monthly charges as long as they are under a certain age - at Commerzbank, for example, this includes students up to the age of 30.

Concerning withdrawing cash, the usual rule in Germany is that it is free to withdraw from your bank’s ATM, but it may cost you to grab a few bills from another location.

However, this is not universally the case. Berlin-favourite Sparkasse, for example, may charge its customers up to €0.50 for withdrawing money from their ATMs, even if they are Sparkasse customers. Other banks, like DKB, offer free withdrawals as long as the cash machine itself doesn’t require a fee.

Digital banking

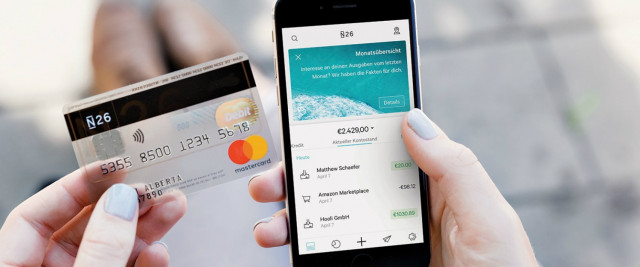

Digital banking isn't for everyone, but banks like N26 can be helpful for starting off in Germany. Photo: DPA

A final thought to consider as you wade your way through all of your bank choices is what you want in your banking experience.

Many across Germany have jumped on the trend of ditching traditional brick-and-mortar banking structures for digital banks like N26 and Comdirect.

While some are wary of the concept of a bank without a building, many of these banks’ customers enjoy the ease of money that is always accessible at the click of a button.

That combined with no-cost ATM withdrawals and lighting-speed customer service are making this new breed of bank a real option for Germany’s expats. N26 is particularly attractive for newcomers, as the site and customer service portal are available entirely in English.

Important to keep in mind, though, is that banks like N26 often do not issue EC-cards, and thus can be difficult to use in many smaller German shops.

Merging your German and international accounts

Assuming you are coming to Germany with existing bank accounts back home, it is good to consider the best way to consolidate before opening your new German account. While there are services like Transferwise that allow international transfers with a fee, some German banks also make it easier to transfer money for their international customers.

Depending on your country of origin, many German banks will have existing partnerships with international institutions that can make the transfer process much easier.

Deutsche Bank, for example, has partnerships with banks like Bank of America (US), Scotiabank (Canada) and Westpac (Australia) that allows money transfers without charging an additional fee.

Also important in starting your banking life are the relationships between the different German banks. Banking partnerships exist between many German banks, allowing you to freely use other ATMs and services without incurring additional fees.

One of the largest examples is the cash group formed between Deutsche Bank, Postbank, Commerzbank and Hypovereinsbank.

Doing the paperwork

Digital banking isn't for everyone, but banks like N26 can be helpful for starting off in Germany. Photo: DPA

A final thought to consider as you wade your way through all of your bank choices is what you want in your banking experience.

Many across Germany have jumped on the trend of ditching traditional brick-and-mortar banking structures for digital banks like N26 and Comdirect.

While some are wary of the concept of a bank without a building, many of these banks’ customers enjoy the ease of money that is always accessible at the click of a button.

That combined with no-cost ATM withdrawals and lighting-speed customer service are making this new breed of bank a real option for Germany’s expats. N26 is particularly attractive for newcomers, as the site and customer service portal are available entirely in English.

Important to keep in mind, though, is that banks like N26 often do not issue EC-cards, and thus can be difficult to use in many smaller German shops.

Merging your German and international accounts

Assuming you are coming to Germany with existing bank accounts back home, it is good to consider the best way to consolidate before opening your new German account. While there are services like Transferwise that allow international transfers with a fee, some German banks also make it easier to transfer money for their international customers.

Depending on your country of origin, many German banks will have existing partnerships with international institutions that can make the transfer process much easier.

Deutsche Bank, for example, has partnerships with banks like Bank of America (US), Scotiabank (Canada) and Westpac (Australia) that allows money transfers without charging an additional fee.

Also important in starting your banking life are the relationships between the different German banks. Banking partnerships exist between many German banks, allowing you to freely use other ATMs and services without incurring additional fees.

One of the largest examples is the cash group formed between Deutsche Bank, Postbank, Commerzbank and Hypovereinsbank.

Doing the paperwork

No surprise: There is a lot of paperwork to fill out when you start banking in Germany. Make sure to bring the right documents with you. Photo: DPA

Now that you know all the prep-work of finding your preferred bank location, it’s time to fill out all of the stacks of paperwork required to get a German Konto. You didn’t really think you would get out of bureaucracy in Germany, did you?

There are some documents you need to have in order to open a bank account.

While this can vary somewhat from bank to bank, the general rule is that you have an Anmeldung, or registration document in your city, proof of income/employment and a valid passport, often asked for with an Aufenthaltstitel, or current German residence permit.

For non-EU citizens, the German residency permit bit can be tricky, as in some cases you first have to possess a German bank account in order to receive an Aufenthaltstitel. If you don’t yet have your residency permit, the best rule of thumb is to meet with your bank individually and discuss your situation.

Starting your banking: Überweisungen (transfers)

You have your fresh, new bank account and now it is time to start spending!

Depending on where you’re coming from, the idea of sending all of your banking information to a company may make you feel a little uneasy - but in Germany, it’s the norm.

For most larger transactions, including things like rent and tax payments, you will be given the IBAN and BIC of your recipient and asked to send the payments directly to their accounts.

While this is not so different from transferring money in most countries, the frequency of this kind of transaction is very much a German invention.

Cash is king

No surprise: There is a lot of paperwork to fill out when you start banking in Germany. Make sure to bring the right documents with you. Photo: DPA

Now that you know all the prep-work of finding your preferred bank location, it’s time to fill out all of the stacks of paperwork required to get a German Konto. You didn’t really think you would get out of bureaucracy in Germany, did you?

There are some documents you need to have in order to open a bank account.

While this can vary somewhat from bank to bank, the general rule is that you have an Anmeldung, or registration document in your city, proof of income/employment and a valid passport, often asked for with an Aufenthaltstitel, or current German residence permit.

For non-EU citizens, the German residency permit bit can be tricky, as in some cases you first have to possess a German bank account in order to receive an Aufenthaltstitel. If you don’t yet have your residency permit, the best rule of thumb is to meet with your bank individually and discuss your situation.

Starting your banking: Überweisungen (transfers)

You have your fresh, new bank account and now it is time to start spending!

Depending on where you’re coming from, the idea of sending all of your banking information to a company may make you feel a little uneasy - but in Germany, it’s the norm.

For most larger transactions, including things like rent and tax payments, you will be given the IBAN and BIC of your recipient and asked to send the payments directly to their accounts.

While this is not so different from transferring money in most countries, the frequency of this kind of transaction is very much a German invention.

Cash is king

Trust us: you'll want to carry a lot of cash around in 'Schland. Photo: DPA

This is a pitfall many new expat fall into, but don’t get caught unaware: you will probably need to have bills on your person at all times. While slowly modernizing, most small business and bars in Germany still only run on Bargeld (cash), and you won’t be able to get around without it.

And it’s not just the small stuff: everything from a wurst to a wardrobe may require you to pay in cash, so you’ll need to have it on hand.

Luckily, Geldautomaten are plentiful in most places in Germany, and are easily recognizable with the EC sign that is usually found on their front.

Our advice: Familiarize yourself with the closest ATMs to your home, office, and favourite locations and you might want to consider taking out larger amounts and storing the rest at home, particularly if your bank takes a fee for cash withdrawals.

Declaring your German account on your home taxes

Having had your German account for a while, you may have left the headache of opening your account in the past. However, there is an important detail for all expats to remember when it comes to foreign bank accounts, and that deals with taxes.

For some countries, you may have to declare all of your foreign bank accounts, including those in Germany, whenever you do taxes.

The general idea with this rule is that you show that you are not hiding money in offshore accounts. For the US, you can contact the International Internal Revenue Service to get advice ahead of time to see what your exact situation looks like.

Trust us: you'll want to carry a lot of cash around in 'Schland. Photo: DPA

This is a pitfall many new expat fall into, but don’t get caught unaware: you will probably need to have bills on your person at all times. While slowly modernizing, most small business and bars in Germany still only run on Bargeld (cash), and you won’t be able to get around without it.

And it’s not just the small stuff: everything from a wurst to a wardrobe may require you to pay in cash, so you’ll need to have it on hand.

Luckily, Geldautomaten are plentiful in most places in Germany, and are easily recognizable with the EC sign that is usually found on their front.

Our advice: Familiarize yourself with the closest ATMs to your home, office, and favourite locations and you might want to consider taking out larger amounts and storing the rest at home, particularly if your bank takes a fee for cash withdrawals.

Declaring your German account on your home taxes

Having had your German account for a while, you may have left the headache of opening your account in the past. However, there is an important detail for all expats to remember when it comes to foreign bank accounts, and that deals with taxes.

For some countries, you may have to declare all of your foreign bank accounts, including those in Germany, whenever you do taxes.

The general idea with this rule is that you show that you are not hiding money in offshore accounts. For the US, you can contact the International Internal Revenue Service to get advice ahead of time to see what your exact situation looks like.

Comments

See Also

This article is available to Members of The Local. Read more Membership Exclusives here.

Germany is a banking powerhouse, with established names like Deutsche Bank, Commerzbank, KfW and DZ Bank all calling Germany home. With these big names, though, come a lot of differences in the banking structure. So how do you know where to start?

We walk you through the ins and outs of making your way through the German banking system.

Know the lingo

The first step to banking is knowing the lingo. Geldautomat, for example, is extremely important: ATM. Photo: DPA

Before you embark on navigating the complicated waters of banking in Germany, it’s important to know the lingo. Here are some of the important German-specific words that you will need to know before you set foot inside a German bank.

EC-Karte – This is an EC card, essentially the same as a debit card, that is the most accepted form of credit payment by most German retailers.

IBAN and BIC- Much like in other places in Europe, your International Bank Account Number (IBAN) and Bank Identifier Code (BIC) are your account number and sort code written in a standard, internationally recognised format. The IBAN starts in Germany with the letters DE, which is the country identifier. Together, your IBAN and BIC will allow you to make international transfers.

Kontonummer– This is your individual account number at your given pack, which will be included as a part of your IBAN number. Equally important to know is your Bankleitzahl (BLZ) – this is your bank routing code, also contained within the IBAN number itself.

Überweisung/Geldüberweisung – This is the word for money transfer, which is how most people in Germany pay for larger bills. More on that later. Important to note in conjunction with this term is TAN codes – special transaction codes that you use online to verify payments from your account.

Picking the right account type

In order to make the right choice about how to begin your banking future in your new home country, it’s crucial to know the types of accounts available to expats in Germany. The two main categories of bank accounts: Girokonto and Sparkonto.

A Girokonto is essentially a checking account. Most transactions are done using this account type, and it works in conjunction with an EC card, as already mentioned. Unlike many countries, Germany does not have personal checks, and thus all transactions done from the Giro account are conducted using either the EC card, cash withdrawals or transfers.

A Sparkonto is the German equivalent of a savings account, and is often opened at the same time as the Giro account (though it can be opened later). This account allows you to save and collect interest.

With a Sparkonto, there is usually a limit on the amount of money you are allowed to withdraw per month, and money is not easily transferred into other accounts.

For both banking types, there are Kontoführungsgebühren, or bank account fees, depending on the institution.

Finding the right bank

With so many banks in Germany, picking the right one means weighing the benefits. Photo: DPA

Armed with your new German banking vocabulary and account knowledge, it’s time to figure out which of Germany’s plethora of banks is the right fit for you.

With so many options out there, it is good to know the big names in the German banking game. While there are many more than the ones below, here are some of the heavy hitters that you may want to keep on your radar.

Deutsche Bank – This is Germany’s largest bank, and is also one of the most well-known internationally. They offer a range of accounts designed for students and also professionals that hold client money in their private accounts. For our American readers, their partnership with Bank of America can make for easy money transfers for customers.

Commerzbank – One of the other large banks in the country, it offers a normal Giro account as well as premium accounts that offer two debit cards and travel insurance. Their site is available in English.

DKB – Deutsche Kredit Bank advertises itself as no/low fees and is an online banking service. It offers a free account and ATM withdrawals (unless that machine charges a fee). Customer support can be contacted via email or through a call centre. The downside perhaps is that they have no physical branches.

Sparkasse – Sparkassen have many branches and ATMs throughout Germany. Each large German city has its own Sparkasse, though in Berlin it is the largest retail/consumer bank in the city. However, they do have higher fees.

Location, location, location

One of the first factors to consider in choosing the right bank is your location in Deutschland. Are you in Berlin, where Sparkasse is the largest banking chain? Or maybe travelling between Frankfurt and Düsseldorf for work? Where you are can have a big affect on what bank is best for you, especially considering the high costs of withdrawing cash at competing banks.

A good rule of thumb in choosing a bank location is to find the three to five banks closest to your home or office, and use those as the start of your search.

Keep in mind that regional offerings, like Landesbank Baden-Württemberg, may not be available in other parts of Germany and might not be a good idea if you plan to travel frequently outside of your area.

Hidden fees

Another key component of selecting the right banking institution is to compare the possible fees. While each bank has its own unique charging rules, the big fees to look for come with age factors, withdrawing money from ATMs and international transfers.

German accounts typically cost around €10 per month in “maintenance fees”, though the exact number varies depending on the bank. Students are largely excempt from these monthly charges as long as they are under a certain age - at Commerzbank, for example, this includes students up to the age of 30.

Concerning withdrawing cash, the usual rule in Germany is that it is free to withdraw from your bank’s ATM, but it may cost you to grab a few bills from another location.

However, this is not universally the case. Berlin-favourite Sparkasse, for example, may charge its customers up to €0.50 for withdrawing money from their ATMs, even if they are Sparkasse customers. Other banks, like DKB, offer free withdrawals as long as the cash machine itself doesn’t require a fee.

Digital banking

Digital banking isn't for everyone, but banks like N26 can be helpful for starting off in Germany. Photo: DPA

A final thought to consider as you wade your way through all of your bank choices is what you want in your banking experience.

Many across Germany have jumped on the trend of ditching traditional brick-and-mortar banking structures for digital banks like N26 and Comdirect.

While some are wary of the concept of a bank without a building, many of these banks’ customers enjoy the ease of money that is always accessible at the click of a button.

That combined with no-cost ATM withdrawals and lighting-speed customer service are making this new breed of bank a real option for Germany’s expats. N26 is particularly attractive for newcomers, as the site and customer service portal are available entirely in English.

Important to keep in mind, though, is that banks like N26 often do not issue EC-cards, and thus can be difficult to use in many smaller German shops.

Merging your German and international accounts

Assuming you are coming to Germany with existing bank accounts back home, it is good to consider the best way to consolidate before opening your new German account. While there are services like Transferwise that allow international transfers with a fee, some German banks also make it easier to transfer money for their international customers.

Depending on your country of origin, many German banks will have existing partnerships with international institutions that can make the transfer process much easier.

Deutsche Bank, for example, has partnerships with banks like Bank of America (US), Scotiabank (Canada) and Westpac (Australia) that allows money transfers without charging an additional fee.

Also important in starting your banking life are the relationships between the different German banks. Banking partnerships exist between many German banks, allowing you to freely use other ATMs and services without incurring additional fees.

One of the largest examples is the cash group formed between Deutsche Bank, Postbank, Commerzbank and Hypovereinsbank.

Doing the paperwork

No surprise: There is a lot of paperwork to fill out when you start banking in Germany. Make sure to bring the right documents with you. Photo: DPA

Now that you know all the prep-work of finding your preferred bank location, it’s time to fill out all of the stacks of paperwork required to get a German Konto. You didn’t really think you would get out of bureaucracy in Germany, did you?

There are some documents you need to have in order to open a bank account.

While this can vary somewhat from bank to bank, the general rule is that you have an Anmeldung, or registration document in your city, proof of income/employment and a valid passport, often asked for with an Aufenthaltstitel, or current German residence permit.

For non-EU citizens, the German residency permit bit can be tricky, as in some cases you first have to possess a German bank account in order to receive an Aufenthaltstitel. If you don’t yet have your residency permit, the best rule of thumb is to meet with your bank individually and discuss your situation.

Starting your banking: Überweisungen (transfers)

You have your fresh, new bank account and now it is time to start spending!

Depending on where you’re coming from, the idea of sending all of your banking information to a company may make you feel a little uneasy - but in Germany, it’s the norm.

For most larger transactions, including things like rent and tax payments, you will be given the IBAN and BIC of your recipient and asked to send the payments directly to their accounts.

While this is not so different from transferring money in most countries, the frequency of this kind of transaction is very much a German invention.

Cash is king

Trust us: you'll want to carry a lot of cash around in 'Schland. Photo: DPA

This is a pitfall many new expat fall into, but don’t get caught unaware: you will probably need to have bills on your person at all times. While slowly modernizing, most small business and bars in Germany still only run on Bargeld (cash), and you won’t be able to get around without it.

And it’s not just the small stuff: everything from a wurst to a wardrobe may require you to pay in cash, so you’ll need to have it on hand.

Luckily, Geldautomaten are plentiful in most places in Germany, and are easily recognizable with the EC sign that is usually found on their front.

Our advice: Familiarize yourself with the closest ATMs to your home, office, and favourite locations and you might want to consider taking out larger amounts and storing the rest at home, particularly if your bank takes a fee for cash withdrawals.

Declaring your German account on your home taxes

Having had your German account for a while, you may have left the headache of opening your account in the past. However, there is an important detail for all expats to remember when it comes to foreign bank accounts, and that deals with taxes.

For some countries, you may have to declare all of your foreign bank accounts, including those in Germany, whenever you do taxes.

The general idea with this rule is that you show that you are not hiding money in offshore accounts. For the US, you can contact the International Internal Revenue Service to get advice ahead of time to see what your exact situation looks like.

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.