Healthcare in Germany: when do you have to pay extra?

You can be certain of a high level of healthcare in Germany. But you’ll also sometimes face additional medical bills – with both public and private insurance.

Understanding the complexities of the two systems takes time. If you’re not sure about the differences between Zuzahlungen (co-payments) and Selbstbehalt (deductibles) who could blame you? (read on for more ...).

From prescriptions to dental work, here’s a handy guide to out-of-pocket healthcare costs – to help you choose the right solution for you.

Find out about ottonova's fully digital insurance solutions for expats

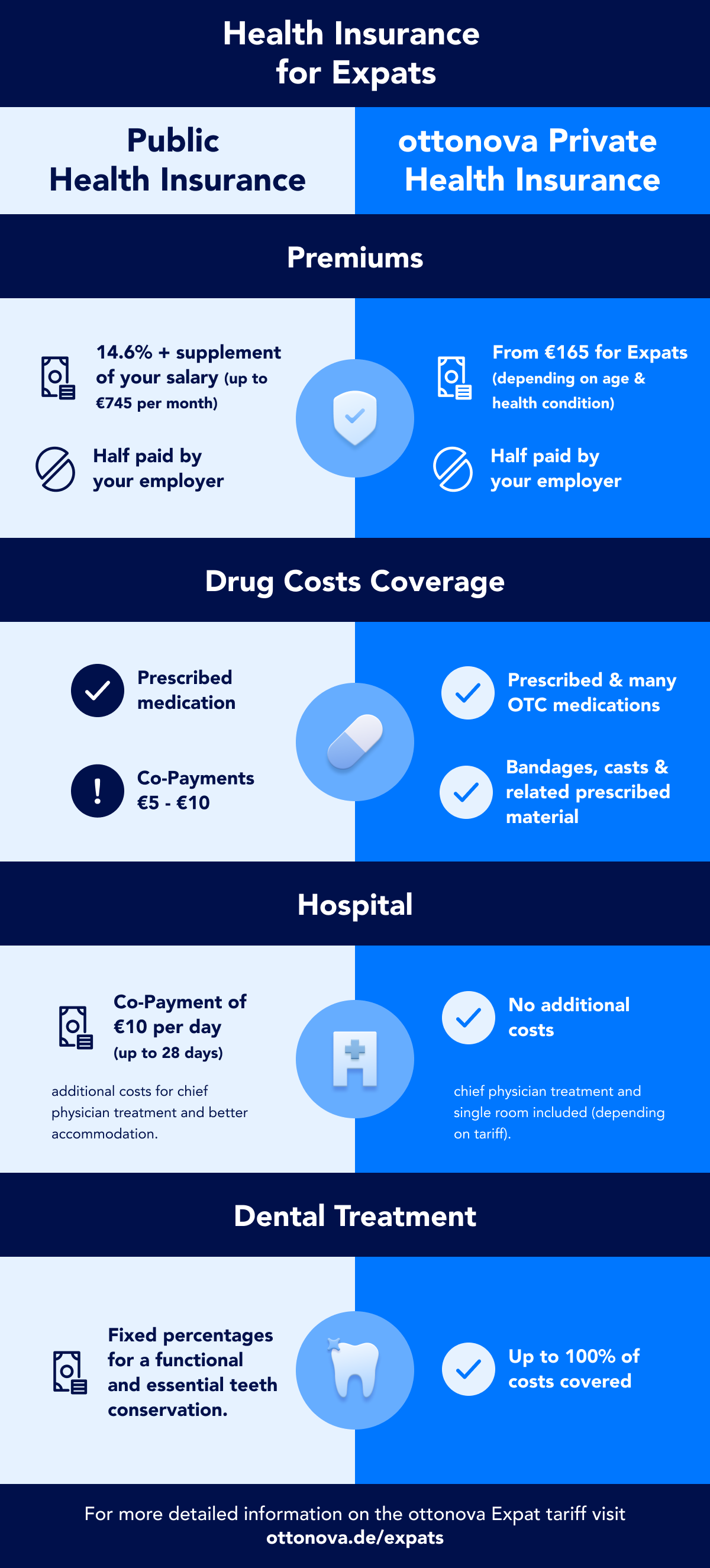

Public or private? First, the basics …

Health insurance is compulsory in Germany. For public health insurance (GKV), everyone pays 14.6 percent of their gross income (plus a small supplement) – and can expect a robust level of protection.

If you’re employed and earn more than €62,550 per year or self-employed, you can choose full private health insurance (PKV). This opens up new choices offering broader coverage of drugs and treatment, including policies from ottonova private health insurance that offer up to 100 percent coverage of all such costs. If you prefer a premium policy, you could consider ottonova’s First Class tariff.

Public co-payments: how you contribute

Perhaps you hoped that having public insurance would mean you only pay your monthly premium? Unfortunately, that’s not the case. Welcome to the world of co-payments – patient contributions that even apply to ambulance transportation costs (although not in emergencies).

After an accident or surgery, you may badly need physiotherapy to get you back to your best. If you’re prescribed a course of treatment with public insurance, you’ll pay 10 percent of the costs – plus a fixed €10 per prescription (which should include multiple sessions).

Private health insurance can offer you much greater coverage – up to 100 percent reimbursement of the charges for physiotherapy.

When you require hospital treatment, you can also expect to pay €10 per day towards this with public insurance (for a maximum of 28 days per year). If you feel in need of extra services or comfort – such as treatment by the head physician or having your own room – you’ll be liable for the full cost, whereas with private insurance you can have such options included in your policy.

Co-payments are limited to a maximum of two percent of annual household income – that’s €1,400 if your gross income is €70,000.

Going private: deciding your deductible

If you go private, you can get the same employer subsidies as with public insurance – up to a maximum of €368 per month – helping to make private coverage more affordable.

You also need to make a choice about your deductible that influences what you pay each month. Your deductible (or excess) is what you pay towards your medical bills before your insurer picks up the remaining amount. Want a lower monthly payment? Just choose a higher deductible.

Fast health insurance services for expats in English – get a consultation with ottonova

Pharmacy payments: just what the doctor ordered?

Even if you’re new in Germany, it’s easy to spot the many pharmacies (Apotheken) – with a green cross or a big red ‘A’. While the German pharmaceutical market is worth more than €43 billion per year, you can only get many medicines from pharmacies with a doctor’s prescription.

Public insurance usually covers prescription-only drugs – but the pharmacy must look for the cheapest option. You’ll also need to make a co-payment of between €5 and €10 per prescription before taking your medicine home for some much-needed rest.

Photo: Getty Images

Photo: Getty Images

Some ‘lifestyle’ drugs are excluded altogether from public coverage: if you’re looking for hair loss treatment, your luck’s out. The same is true if you’re fond of herbal remedies; many appear on the Ministry of Health’s list of drugs you can’t claim for – along with treatments you can buy over-the-counter (OTC) like cold medicines, Ibuprofen and nasal sprays.

But some private companies do partly or fully cover OTC drugs. With , it’s easy to get many such medicines reimbursed regardless of the supplier or price of the drug – just scan your receipt and upload it in the app. Need a quick answer on whether a particular drug is covered? Just ask the English-speaking Concierge in the app or by calling while in the pharmacy.

Dental bills: avoiding a kick in the teeth ...

Many people dread a simple trip to the dentist – let alone root canal surgery. But taking out private insurance that covers the costs of complex dental treatment could help you avoid additional financial pain.

With public insurance, you’ll generally be covered for check-ups and basic dental, gum and orthodontic treatment. You’re less likely to be fully covered for annual dental cleaning, which helps prevent gum disease – as well as keeping your teeth whiter.

With major dental treatments, relying on public insurance could mean you have to pay up to 80 percent of the cost. If you need dental prosthetics, for example, you must share a treatment and cost plan from your dentist with your insurer – who then decides what it will pay.

As an example, endodontic treatment – involving the soft pulp inside the tooth – could cost around €1,300 with public insurance typically covering around €350. That would leave you with €950 to pay – money that could be covered in full with the right private policy. If you have GKV insurance, you can always take out a private top-up such as those offered by ottonova.

Digital reimbursement: get your money back fast!

Even with many private insurers, you may have to pay up for healthcare costs first and then wait for them to process the claim and transfer the money to your bank account. The paperwork can also be a drag to deal with.

As Germany's first fully digital private health insurer, ottonova is often able to send the money to your account before the bill becomes due. Bills of up to €500 uploaded to the app will be reimbursed within 48 hours from Monday to Friday. See the infographic below for more details of how ottonova's health insurance for expats compares with public health insurance.

This content was paid for by an advertiser and produced by The Local's Creative Studio.

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.